Wed 15 / 01 / 14

A year in data by Thomas Perrigo

This week’s blog is taken from Thomas Perrigo’s article in the recent Economic Development Bulletin.

In 2010 the CESP set a target of 6,000 new jobs being required by 2014 ‘simply in order to maintain the current employmment rate’. Our 3 year rolling figure is currently 120 above this, so we are well on track. Also the employment rate has gone up by 0.2%.

Over the course of 2012 we also saw the employment rate rise due to new job creation, alongside falls in the number of people claiming JSA.

The explanation for how the unemployment rate can be rising at the same time as the employment rate is relatively simple.

The explanation is that the ‘economic inactivity rate’ is falling, meaning that more people are entering the labour market (typically, during a recession, economic activity rates decline[3]) and so this increase in activity can be taken as a further measure of the fact that we are moving out of economic recession.

Over the past few years, activity rates have increased by 5,800 people, and the fall in economic inactivity is coming from full-time students deciding to work, or looking for work, during study. Students cannot claim JSA, and so where they do not find employment, or they are between short-term positions perhaps only held during holidays, they would be counted as unemployed.

4,800 of the 5,800 extra people who have entered the labour market in the two years to 2012 are previously inactive full-time students. We are observing falling JSA claims and rising unemployment figures it is more likely the case that the figures are telling us that it is primarily undergraduate students who are driving up the unemployment figures, otherwise we would see upward pressure on JSA claims.

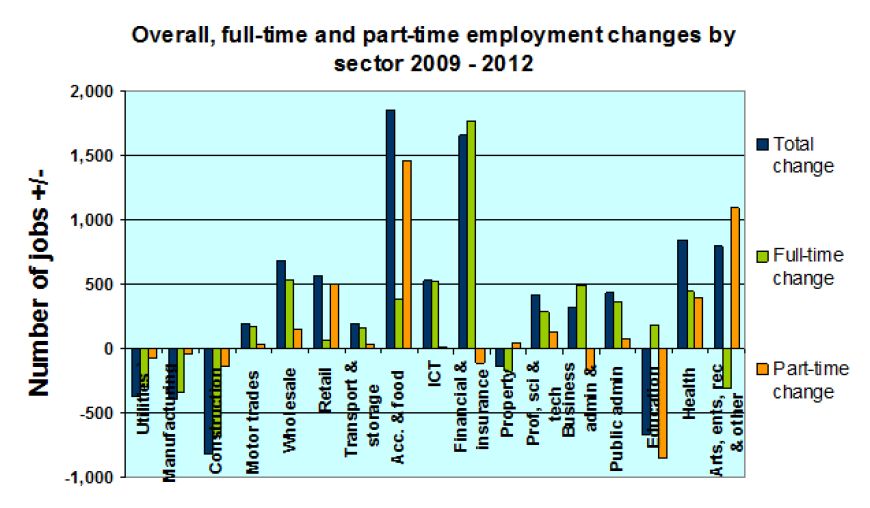

Previous to the latest release of BRES data, job growth in the city was relatively strong, but was worryingly concentrated towards part-time work, with only a minority of new jobs being full-time[4]. This trend has reversed according to the latest data, with the vast majority of new jobs in 2012 being full-time, and also broadly with a strong proportion in sectors which provide higher paid and skilled jobs[5].

As a result of creating 6,120 jobs over the three years to 2012 the city employment rate has risen by 0.5%[6].

Population growth in the city is driven primarily by working age population growth, such as the expansion of the two Universities’ undergraduate intake, graduate retention and the fact that the city attracts skilled workers from other areas.

It is likely that the increasing prevalence of part-time and more flexible work reflects the increasing demand from both students and EU workers for this kind of work, which allows the business to reduce overheads associated with more formal permanent contract employment, and also benefit from a surplus of labour demanding this work. This helps reduce the wage-cost structure for businesses making them more competitive.

On the other side of the labour market coin, we can also see strong growth in knowledge focussed businesses offering full-time and skilled positions to more qualified workers. Many of these businesses favour the city centre due to the benefits of agglomeration[7], and the proximity to services, amenities and cultural activities. This in turn creates vitality and demand for services in the city centre.

Recent GVA data, however, has shown a relatively strong bounce in 2012 with per-head growth of just over 2%, and total economic growth of just over 3%, compared to overall UK per capita growth of 0.8% and total growth of 2%.

‘Production’ in the economy has lost significant GVA over the past few years, and also that employment in primary sectors is declining in general. It is well recognised that Brighton & Hove has a highly service oriented economy, and that the city has been increasingly specialised away from primary production, however, this does raise issues for workers losing their jobs in these areas in terms of re-skilling and adapting to new types of employment.

The idea that we may be specialising towards an increasingly services oriented economy is a challenge in terms of the sectoral shifts which have in the past caused some level of structural unemployment in the UK, which can be observed to some extent in Brighton & Hove. However, with the increasing specialisation in high end knowledge services and digital technology, combining with new technology and techniques in production such as 3d printing, it may also be possible for the city to capitalise on forms of production and manufacturing which can capitalise on the human capital, business sectors and benefit from agglomeration in the city centre.

[2] ONS data is often ‘lagged’ by at least 12 months due to the method of collection and analysis. Indicative data for 2013, available from Duport.co.uk also shows very strong business formation.

[3] More people have children during economic downturns; more people choose study as a route to upskilling and re-positioning themselves… etc.

[4]http://www.brighton-hove.gov.uk/sites/brighton-hove.gov.uk/files/Economic%20Development%20Bulletin%20-%20September%202013%20v2.pdf

[7] Agglomeration refers to the economic benefits of co-locating next to suppliers and customers, and the idea that more ‘dense’ economies are more productive, pay higher wages, and that this can create more self-sustaining growth.

You might also like:

If you want to contribute to the Chamber blog, contact us on hannah@brightonchamber.co.uk